Digital Fraud Wiki

Your source for the latest fraud intelligence, insights, research, and commentary.

Anti-money Laundering (AML): Rules for Catching Financial Crime

Every year, somewhere between $800 billion and $2 trillion dollars is laundered by criminals by law enforcement. What’s worse, more than 90% of money laundering isn’t caught. That’s why regulations require anti-money laundering (AML) at all financial institutions.

In this wiki we’ll explain everything you need to know about AML.

What is Anti-Money Laundering?

Anti-Money Laundering (AML) is a program financial institutions follow to stop money laundering activities. AML also commonly refers to the set of laws they must follow to create that program. AML regulations mandate institutions actively monitor for, prevent, detect, and report money laundering and related criminal activity. These rules also include taking the same measures against terrorist financing.

The Financial Action Task Force (FATF), an intergovernmental organization, sets global standards for AML and Countering the Financing of Terrorism (CFT). These guidelines help financial institutions, including banks and money services businesses, to identify suspicious activities such as structuring, where transactions are broken down to avoid detection thresholds like those requiring a Currency Transaction Report (CTR). The U.S. Department of the Treasury and similar bodies in the European Union enforce these standards, ensuring compliance across financial sectors.

Anti-Money Laundering Compliance

AML regulations require financial institutions to verify the identities of beneficial owners and monitor transactions involving politically exposed persons (PEPs) who may present higher risks due to their positions of influence. Financial Intelligence Units (FIUs) collect and analyze information about transactions that may indicate money laundering or terrorist financing. Compliance measures, such as filing CTRs for large cash deposits or withdrawals, help trace the flow of funds through bank accounts and other financial services providers. The cooperation of nations, including the United Nations and regional bodies, plays a vital role in strengthening AML frameworks globally.

Under AML regulations and anti-money laundering laws, financial institutions legally must have certain capabilities, and many implement an AML compliance program to ensure the laws that mandate different parts of AML are enforced.

Here’s an overview of key AML regulations:

Anti-Money Laundering Act (AMLA) is a set of laws and regulations designed to prevent and combat money laundering and the financing of terrorism. It aims to detect and deter the movement of illegally obtained funds through financial systems.

Under the AMLA, financial institutions must:

- Implement customer due diligence

- Report suspicious activities

- Implement recordkeeping

- Establish internal controls to ensure compliance.

The AMLA enhances oversight and enforcement capabilities, imposes penalties for violations, and promotes international cooperation in the fight against financial crimes.

The Bank Secrecy Act (BSA) mandates AML must have:

- Internal controls, policies, and procedures

- A designated AML compliance officer

- Ongoing employee training

- Independent testing

The USA Patriot Act, which expands the scope of the BSA, mandates AML must:

- Include customer identification programs, including know your customer (KYC)

- Have enhanced due diligence for high-risk customers

- Report suspicious activity to the Financial Crimes Enforcement Network (FinCEN)

Under the Office of Foreign Assets Control (OFAC) Regulations, AML must enforce OFAC, economic, and trade sanctions. This includes those against targeted foreign countries, terrorists, international drug traffickers, and other illegal activities.

Finally, as part of Customer Due Diligence (CDD) requirements, FinCEN requires AML must:

- Collect and verify beneficial ownership information for legal entity customers

- Conduct ongoing monitoring of customer information and transactions

- Make risk assessments

These regulations aren’t limited to banks and traditional financial institutions. FinCEN issues AML regulations for money services, casinos, precious metals, stones, and jewelry dealers too.

Noncompliance with AML regulations set forth by law enforcement agencies and can result in significant fines and even legal action.

How Does Anti-Money Laundering Work?

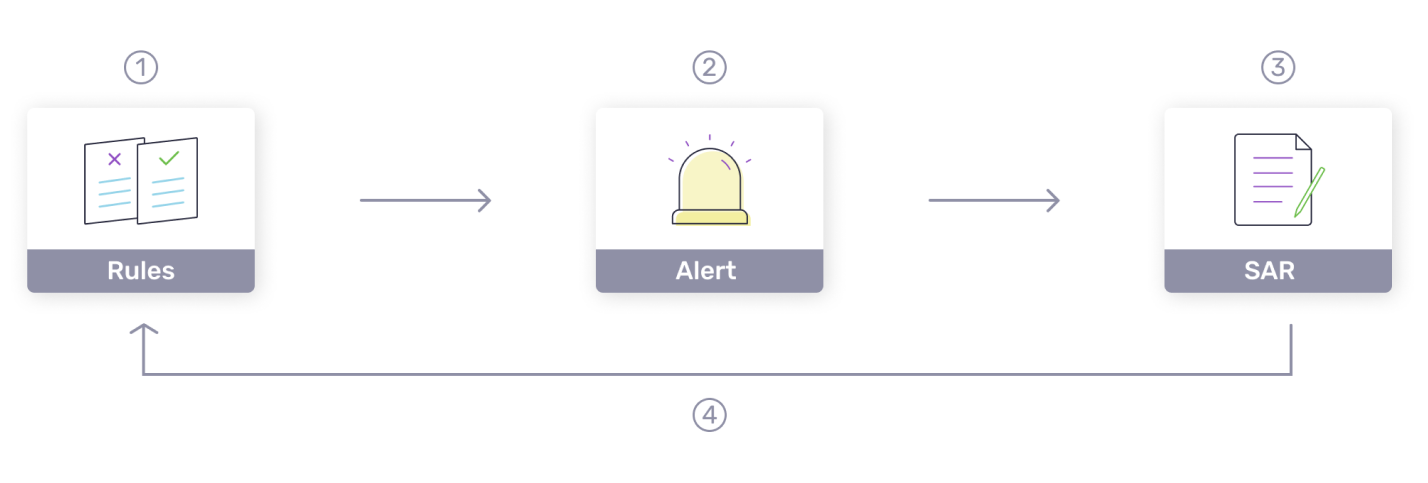

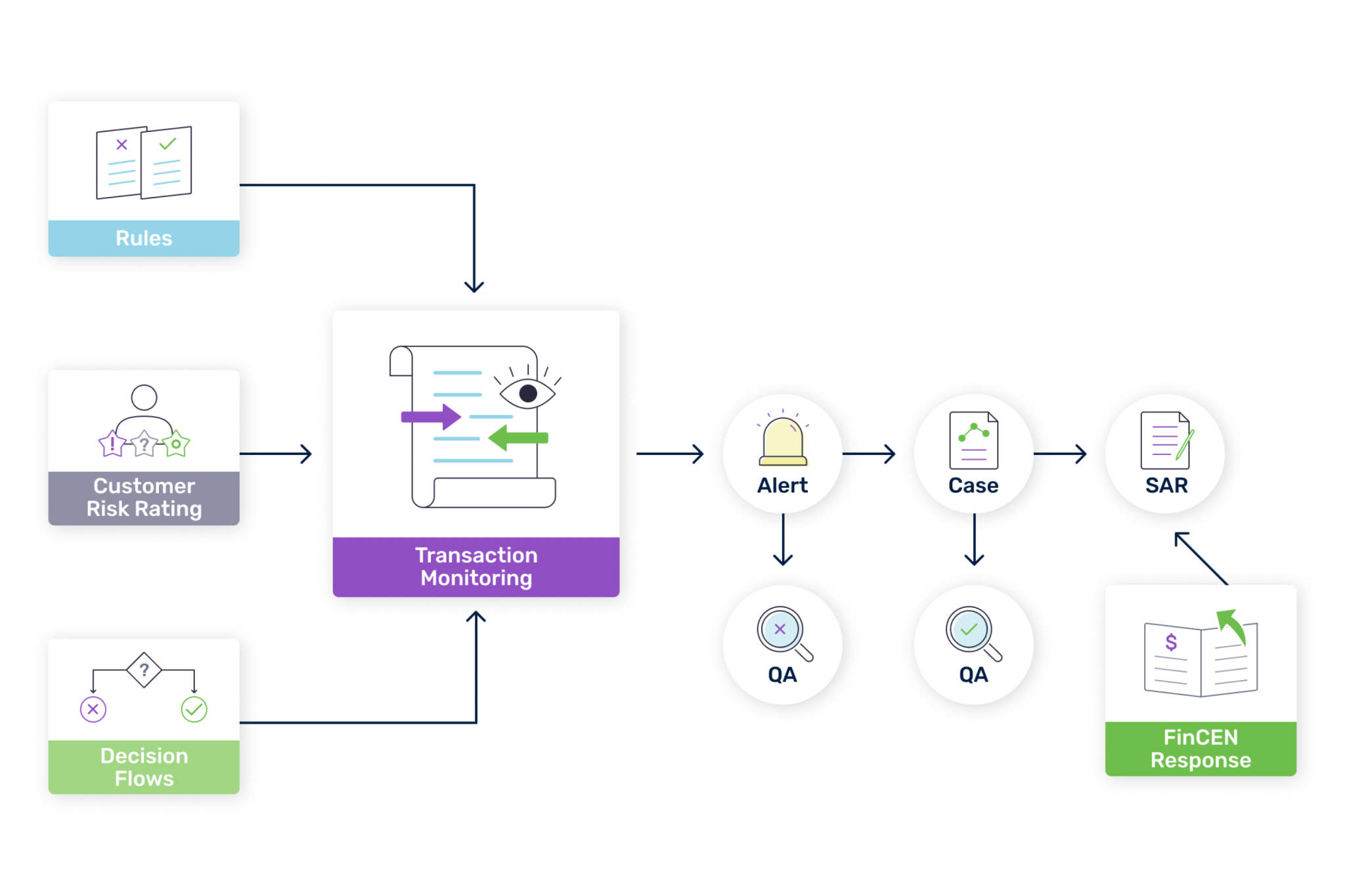

Traditional rules-based AML systems use predefined scenarios or “rules” to identify suspicious transactions and activities. These systems first analyze huge volumes of transactional data. Then they identify any transactions that meet the rules indicating money laundering and flag them. Flagged transactions go to a fraud investigator for further review as part of the case management process.

Traditional rules-based AML systems follow a similar framework:

- Systems analyze transactional data for scenarios that break the “rules” and flag them.

- Transactions that meet the predefined rules generate alerts and flag the activity as suspicious.

- AML analysts investigate to determine if the transaction is unlawful. If it is, the analyst may file a suspicious activity report (SAR) with regulatory authorities.

- Predefined rules are regularly updated based on new data and feedback to improve the accuracy of the system.

This process detects layering money laundering and placement by catching strange behavior and illicit activity. In some cases, it can also detect money laundering past the integration phase if a criminal makes an irregular transaction.

The fight against money laundering is a challenging one. Although traditional rules-based AML systems are effective, they have limitations. Chief among them is generating a high number of false positives. These require significant time and resources to investigate, and can often degrade customer experience and impact customer relationships. Older rules-based systems also struggle to identify new and emerging patterns of money laundering or organized crime rings.

What is AML Transaction Monitoring?

AML transaction monitoring is the actual process an AML system follows to detect patterns of money laundering. It involves all the steps listed above, and is a key component of any AML system.

In recent years, AI and machine learning have boosted AML transaction monitoring capabilities. Some transaction monitoring systems, like DataVisor’s, detect suspicious transactions in milliseconds.

Learn more about AML transaction monitoring from a CPO’s perspective

What is Anti-money Laundering Certification?

AML certifications are credentials awarded to individuals who prove expertise in AML compliance.

Certified Anti-Money Laundering Specialist (CAMS)

The most recognized AML certification globally, CAMS certifies advanced knowledge in detecting and preventing money laundering.

Certified Fraud Examiner (CFE)

Granted by the Association of Certified Fraud Examiners (ACFE), CFE equips professionals with knowledge to investigate and prevent fraud and corruption, complementing AML.

Certified Financial Crime Specialist (CFCS)

A broader credential, CFCS is suited for professionals across AML, fraud, and compliance fields, providing skills to handle complex financial crime investigations.

AML certifications provide validation of expertise in AML compliance — ideal for professionals in compliance, fraud, and regulatory roles.

Who needs an anti-money laundering certificate?

AML certification benefits any professional working in risk management, regulatory compliance, or fraud operations.

While they’re not always required by law, its common for employers to require or prefer AML-certified staff. Regulators often mandate that institutions have a certain number of AML-certified staff members.

If you prefer to download this overview, here it is: AML Policies and Regulations Overview Sheet as a PDF.

Modern anti-money laundering using artificial intelligence

AI and machine learning have upgraded AML by making it both cheaper and more effective. These algorithms analyze massive volumes of data far exceeding what traditional rules systems can do. They also detect suspicious patterns much faster and more accurately. Plus, reduced false positives and fewer manual reviews help institutions get more on their investment.

AI and ML can also assess the risk of money laundering associated with individual transactions or customers. They analyze historical data, customer behavior, and digital fingerprints to assign risk scores to financial transactions. These help focus investigations and trigger enhanced due diligence measures.

AI is always learning and adapting to new patterns of money laundering, so its accuracy over time improves, too, helping to improve anti-money laundering programs. With money laundering techniques evolving rapidly, this is particularly important.

Anti-money laundering with DataVisor

DataVisor’s AML platform leverages a best-in-class AI-powered platform to :

- Surface unknown crimes and uplift threat detection by over 35%

- Help organizations comply with anti-money laundering regulations

- Reduce false positives by over 50%

- Enhance identity resolution with data enrichment and linkage analysis

- Boost productivity by 10x with alert triage and prioritization

Get a personalized demo of how DataVisor can revolutionize your AML solution by speaking with one of our experts.